In recent OpenFalklands posts, we discussed the Chris Doyle, 2006 telecommunications report, the 2016 Cartesian telecommunications report and the resultant 2017 Communications Ordinance. It’s now time to look at some of the impacts on the Falkland Islands’ telecommunications landscape as experienced by consumers and businesses in their everyday communication activities over the last decade. Of course, it is not possible to address every change in a short post like this.

Improvements since 2016

The hiring of a Communications Regulator

The first significant institutional development was the appointment of a full-time Communications Regulator in 2017, marking the first time the sector had dedicated oversight with defined responsibilities. There have been four regulators since 2017, with a long period during which the role was undertaken by the Attorney General. Over time, this led to the creation of an active regulatory system, including compliance monitoring, complaints and fault reporting, KPI data collection, customer satisfaction surveys, and enforcement powers. This brought greater transparency and accountability to the sector, even if many of these changes were not directly visible to everyday users.

Spectrum management regime

The introduction of a formal spectrum management regime has managed the use of radio frequencies. This includes developing an ITU-standard-based national frequency allocation table and establishing a structured licensing framework. Together, these measures have brought the Falkland Islands more closely into line with international best practice, while providing a solid foundation for both future technologies and existing licence-exempt services such as Wi-Fi.

FIG’s £1m/year Intelsat satellite capacity subsidy.

Since the introduction of the Communications Ordinance, there have been clear improvements in the Falkland Islands’ overall telecommunications satellite capacity. A major step change came in late October 2019, driven by sustained public investment, with FIG funding of around £1 million per year from 2019 to increase satellite capacity. This initially delivered a 97% increase in international capacity and a doubling of data allowances. It was also claimed that congestion had significantly decreased due to improved contention ratios, but this claim was contested at the time. This investment directly improved day-to-day performance for consumers and businesses, judging by a perceived reduction in complaints. Overall international bandwidth had already increased by over 300% since 2015, leading to faster, more reliable broadband than previously available. In 2025, the Public Accounts Committee investigated whether this £8 million of ongoing government expenditure investment was justified – Falklands Telecomms: £8 Million Broadband Spend: Sure SA and FIG Under Scrutiny

Sure’s Intelsat capacity was increased by 45% again in 2022.

Sure’s second Intelsat earth station

Sure added a second Intelsat earth station dish as part of a wider upgrade to its telecommunications infrastructure. Installation of the additional geostationary satellite antenna was completed by October 2023, significantly increasing broadband satellite capacity to 220.5 Mbit/s and total capacity to 554 Mbit/s.

This upgrade marked a major improvement in service resilience for the Falkland Islands, which had previously relied on a single Intelsat earth station link for many years. With the introduction of the second dish, traffic could be distributed between two antennas, approximately 9 m and 11 m in size, resulting in a substantial boost in capacity and resilience.

4G mobile network deployment

There have also been important infrastructure upgrades, most notably the rollout of the 4G mobile network announced by Sure on the 14th December 2018. This marked a significant step forward over the previous 2G mobile service, enabling faster data speeds, improved reliability, and a much better overall user experience. For the first time, many residents were able to make full use of modern smartphones for everyday tasks such as messaging apps, email, navigation, and streaming. Coverage was expanded across Stanley, Mount Pleasant and parts of Camp. While still considerably constrained by underlying data capacity limits, the introduction of 4G represented a clear and tangible improvement in mobile capability and brought the Islands a little closer to contemporary global standards.

However, the quality of service for 4G Falklands voice calls on the 4G mobile network is arguably compromised because they were still routed over the existing 2G infrastructure using ‘Circuit Switched Fall-back‘ (CSFB) technology. The 4G network could be upgraded to use Voice over LTE (VoLTE) – a standard approved in 2012 – which would completely remove the fallback to 2G. It is understood that this has not been undertaken. It could be asked why, with the widespread use of smartphones and fewer legacy 2G mobiles, this has not happened. (Note: if I am wrong about this, please let me know.)

Starlink Approval

Most significantly, the eventual approval of low Earth orbit satellite services such as Starlink in 2025 marked a step change in telecommunications innovation in the Falkland Islands. For the first time, users had access to an alternative source of high-speed, low-latency connectivity independent of the existing centrally managed Sure broadband service. This development arguably represents the most impactful change in the history of telecommunications in the Islands, fundamentally altering both the technical and competitive landscape now and in the future.

Notably, this shift occurred despite the longstanding constraints of the Communications Ordinance, which had historically limited self-provision of VSAT services. The approval of LEO services, therefore, reflects not only a technological breakthrough but also a significant regulatory evolution. It challenged many of the assumptions underpinning earlier policy and ordinance frameworks, particularly those based on centralised control, and the need to tightly manage international connectivity, and opened the door to a more decentralised and resilient communications environment going forward.

Sure’s network upgrades

From Sure’s perspective, additional positives could also be identified beyond those most visible to consumers. Sure would likely highlight improvements in network resilience and reliability, including better uptime, fault management, and peak-demand handling. While less visible, these are essential in a remote and capacity-constrained environment.

There has also been ongoing modernisation of core infrastructure in Stanley and LTE technology in Camp, alongside improved traffic and capacity management. These changes have helped make more efficient use of limited resources and supported a more consistent user experience over time. However, a major fibre or 5G upgrade to the Stanley broadband infrastructure is now well overdue, as is widely recognised. Also, with the now widespread use of Starlink in Camp, a major strategy overhaul is now becoming mandatory.

Sure has also invested in its own LEO satellite service, based on OneWeb’s low Earth orbit (LEO) satellite network. Although it was initially announced for introduction in late 2023, the deployment does not appear to have established a clear role in the Falkland Islands. Installations have been limited, and the service is not currently listed as available on Sure’s website.

In February 2021, EXCO approved the purchase of 12 network probes (6 mobile, 6 fixed) to be deployed in Stanley and Camp to monitor broadband speeds and network availability. Following the contract and acquisition, all 12 probes were deployed by January 2022. As Sure benefits from the data provided by the probes, they contributed 25% of the capital costs. The benefits of these probe initiatives for broadband download speed KPIs – even with the latest probe strategy outlined in 2016 – are highly questionable. More on this soon on OpenFalkalnds.

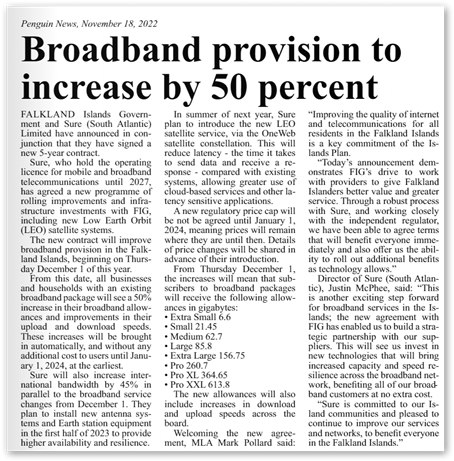

No more broadband quotas!

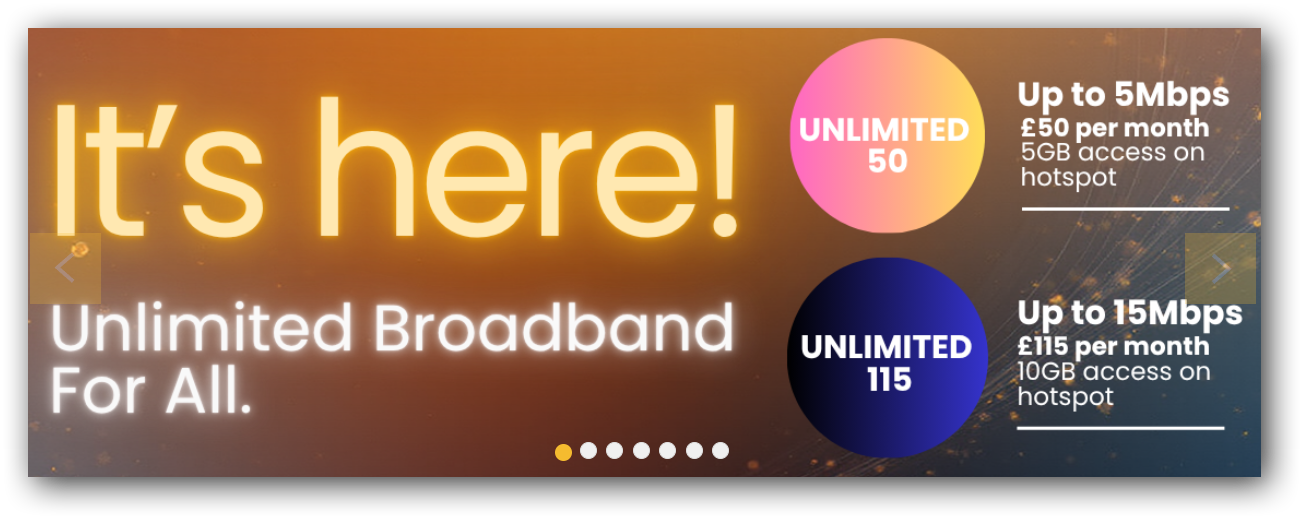

A fundamental shift finally came in January 2026 with the end of the monthly broadband quota regime, which had been in place for well over a decade. The introduction of two “unlimited” services marked a long-overdue change in how internet access was structured in the Falklands. While presented as a natural evolution of the market, this shift likely reflected the growing pressure from the approval and uptake of Starlink.

Furthermore, following FIG Starlink approval, Sure increased its line rental from £12 to £30 per month for customers without a Sure broadband package, presumably to help offset the loss of home broadband revenue. There are still usage quotas on hotspots, and upload speeds are fixed at 1 Mbit/s.

MiPlayer streaming

In 2020, the Falkland Islands Government approved the introduction of MiPlayer, a system developed by BFBS to deliver live and catch-up television and radio services to military staff in remote locations. Following a successful trial period, the service was rolled out to residents, providing access to live channels and on-demand content across a range of devices, including smartphones, tablets, and televisions.

Importantly, MiPlayer was designed to operate without consuming users’ data allowances, making it a practical solution within the Islands’ constrained bandwidth environment.

Undersea Cable

Undersea cable connectivity has long been explored as a potential step-change solution for the Falkland Islands, offering significantly increased bandwidth, lower latency, and greater long-term resilience compared to satellite-based systems. The successful connection of St Helena to Google’s Equiano cable notably raised both hopes and expectations that a similar solution might one day be achievable for the Falklands.

In 2019, the Falkland Islands Government (FIG) confirmed that fibre-optic cable options were under strategic review alongside emerging satellite technologies, with preliminary discussions held with potential providers, including those facilitated through Sure’s offices in Guernsey. However, the high capital costs, complex logistics, and limited commercial returns associated with such a remote deployment have consistently posed major financial barriers. Ultimately, it was concluded that expanding satellite capacity was the most viable near-term solution.

More recent discussions have introduced a different dimension, based on Peraton’s “Southern View” concept, which is understood to have explored integrated communications solutions that could potentially incorporate a subsea cable as part of a broader, security-focused architecture. While public details remained limited, this type of proposal suggests a shift away from purely commercial models towards more strategic or government-aligned infrastructure approaches.

However, such concepts now appear to have lost momentum, likely reflecting financial constraints, shifting global priorities, and the rapid advancement of satellite technologies. While an undersea cable remains technically feasible, and the long-term benefits are clear, it is probably not currently considered a near-term prospect—though, as ever, it cannot be ruled out entirely.

Persistent Challenges

Persistent Challenges

Despite the major improvements discussed, many of the core concerns raised in the 2006 and 2016 reports have persisted. Costs remain high by global standards, and affordability remains a major issue for both consumers and businesses. Notably, many of the improvements, particularly the 2019 increases in satellite capacity, were achieved only with significant public subsidies, highlighting the system’s underlying cost challenges.

The reliance on a single licensed provider has continued to limit competition and choice. The policy of discouraging self-provision, particularly through high VSAT licensing fees, has constrained alternatives for many users and reinforced the dominance of the existing model. This only changed with the 2024 Starlink petition, which focused on Starlink service approval and a reduction in licence costs from £5,400 to £180.

There has also been continued scepticism about the effectiveness and independence of regulation. While the framework now exists, and important groundwork has been laid, questions remain about whether it has been sufficiently resourced or empowered to drive meaningful change in pricing and service quality.

Finally, there is a broader concern that policy has at times struggled to keep pace with technological change. The delay in embracing newer services such as Starlink highlighted the tension between maintaining a controlled system and enabling access to emerging global technologies.

Finally, it also seems that the ambition to host an annual public Communications Week as part of 2020’s National Broadband Strategy has been forgotten, which was quite a disappointment for many.

Overall

The decade since 2016 has delivered clear progress in capacity, structure, and capability, supported largely by public investment and the development of a functioning regulatory system. However, many of the underlying tensions identified at the time remain unresolved. The result is a system that is stronger and more modern, but still shaped by familiar trade-offs between control and competition.

The major defining moment of the decade was the 2024 public petition advocating approval of Starlink services and reform of VSAT licensing costs. This marked a significant shift, as public pressure directly influenced telecommunications policy. The outcome not only enabled access to low Earth orbit satellite services but also challenged long-standing assumptions around centralised control and restrictions on self-provision, accelerating the move towards a more open and diversified communications environment.

Perhaps, if lessons have been learned, the 2026 telecommunications strategy report by Cambridge Management Consulting will focus less on selecting a single model and more on how multiple approaches can coexist. The key question is no longer whether to adopt a monopoly or a competitive model, but how to manage a hybrid system in which traditional infrastructure and emerging technologies coexist.

Regulation must adapt to this more complex environment, with greater emphasis on fairness, transparency, and ensuring all users benefit from new developments. At the same time, the need for significant CAPEX investment in telecommunications infrastructure in Camp and Stanley, and clarity over how it will be funded, remains, particularly for mobile coverage.

In this sense, 2026 does not mark the end of earlier issues, but it does represent a turning point. The Falklands are no longer dependent on a single telecommunications model, and the challenge now is to make the most of a more diverse and evolving technological landscape.

Chris Gare, OpenFalklands, March 2026, copyright OpenFalklands